What is the definition, scope, and significance of the Asia Pacific FPGA Security Market?

The Asia Pacific FPGA Security Market encompasses the design, deployment, and management of field‑programmable gate array solutions that incorporate hardware‑level security features such as bitstream encryption, secure boot, and tamper detection across the region. Its scope spans telecommunications, consumer electronics, data centers, military and aerospace, industrial, automotive, and other end‑user segments, reflecting the growing need for trusted programmable logic in critical infrastructure. The market’s significance lies in enabling secure, reconfigurable computing that supports emerging applications like 5G, AI acceleration, and autonomous systems while meeting stringent regulatory and compliance requirements.

What are the key drivers, restraints, challenges, and opportunities shaping the Asia Pacific FPGA Security Market?

Primary drivers include rising cyber‑threat sophistication, rapid 5G rollout, increasing adoption of AI workloads, and government mandates for hardware root‑of‑trust in defense and critical infrastructure. Restraints involve high development costs, limited skilled talent, and lengthy qualification cycles for secure FPGA designs. Challenges center on supply‑chain vulnerabilities, evolving attack vectors such as side‑channel analysis, and the need for standardized security certification across countries. Opportunities arise from growing demand for low‑power secure edge devices, expansion of cloud‑based FPGA services, and strategic partnerships between semiconductor vendors and regional system integrators.

What current and emerging growth trends are influencing the Asia Pacific FPGA Security Market?

Key trends include the shift toward heterogeneous computing platforms that combine secure FPGAs with CPUs and GPUs, adoption of SRAM‑based FPGAs with built‑in anti‑tamper features, and increasing use of flash‑based devices for non‑volatile secure key storage. The market also sees rising interest in high‑end FPGA configurations for data‑center acceleration, mid‑range devices for industrial IoT gateways, and low‑end parts for cost‑sensitive consumer electronics. Additionally, open‑source hardware security frameworks and regional standardization efforts are accelerating time‑to‑market for secure programmable solutions.

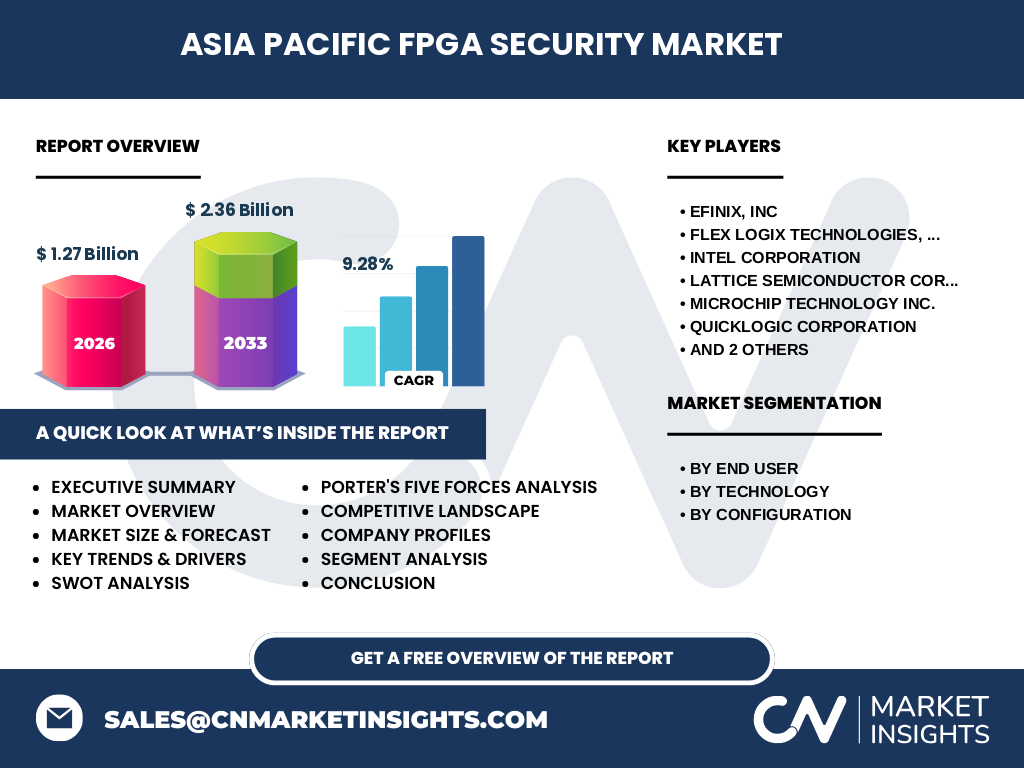

How did COVID‑19 impact the Asia Pacific FPGA Security Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains and delayed project deployments, especially in automotive and industrial segments, causing a short‑term dip in demand for secure FPGA solutions. However, accelerated digital transformation, remote‑work infrastructure upgrades, and heightened focus on resilient communications spurred renewed investment in secure programmable logic from 2021 onward. The recovery trajectory shows a steady rebound, with the market reaching a size of 1.27 billion in 2026 and projected to grow to 2.36 billion by 2033, reflecting a compound annual growth rate of 9.28 percent.

Who are the major competitors and how consolidated is the Asia Pacific FPGA Security Market?

The competitive landscape is dominated by a handful of global semiconductor leaders and emerging regional players. Key companies include Efinix, Inc., Flex Logix Technologies, Inc., Intel Corporation, Lattice Semiconductor Corporation, Microchip Technology Inc., QuickLogic Corporation, S2C, and Xilinx, Inc. Market consolidation is moderate; while the top tier holds significant share through extensive product portfolios and strong R&D, niche vendors differentiate via specialized low‑power or high‑security configurations, creating a dynamic ecosystem with both collaboration and competition.

What are the high‑level findings and key takeaways from the Asia Pacific FPGA Security Market executive summary?

The executive summary highlights that the Asia Pacific FPGA Security Market is poised for robust expansion, driven by escalating security requirements across telecommunications, data centers, defense, and automotive sectors. The market size of 1.27 billion in 2026 is expected to more than double to 2.36 billion by 2033 at a 9.28 percent CAGR. Segmentation by end user, technology (SRAM, flash, antifuse), and configuration (low‑end, mid‑range, high‑end) reveals diverse growth pockets. Strategic investments in secure IP, regional partnerships, and certification readiness are critical for stakeholders aiming to capture emerging opportunities.

What are the market projections for the Asia Pacific FPGA Security Market from 2025 to 2032?

Forecasts indicate the market will expand from a base of 1.27 billion in 2026 to approximately 2.36 billion by 2033, implying a consistent compound annual growth rate of 9.28 percent throughout the period. Growth is expected to be strongest in high‑end FPGA configurations serving data‑center and AI acceleration workloads, while mid‑range and low‑end segments will benefit from industrial IoT and automotive secure electronics adoption. The projection assumes continued investment in secure silicon IP and favorable regulatory environments across major Asia Pacific economies.

How is the Asia Pacific FPGA Security Market sized and shared across its segmentation categories?

The market is segmented by end user into telecommunications, consumer electronics, data centers and computing, military and aerospace, industrial, automotive, and other end users, each contributing to the overall 1.27 billion valuation in 2026. Technology segmentation covers SRAM, flash, and antifuse FPGAs, with SRAM devices leading in high‑performance secure applications. Configuration segmentation divides the market into low‑end, mid‑range, and high‑end FPGAs, reflecting varying performance, power, and security requirements across verticals. Detailed share breakdowns are provided in the full report.

What is the geographic distribution of the Asia Pacific FPGA Security Market on a global scale?

Globally, the Asia Pacific region represents a significant and fast‑growing portion of the overall FPGA security market, driven by large‑scale 5G deployments, expanding data‑center infrastructure, and strong defense modernization programs in countries such as China, Japan, South Korea, India, and Australia. While exact regional revenue splits are detailed in the comprehensive study, the region’s aggregate market size of 1.27 billion in 2026 underscores its pivotal role in the worldwide secure programmable logic landscape.

How does each major Asia Pacific sub‑region perform in the FPGA Security Market?

Regional analysis shows that East Asia, led by China, Japan, and South Korea, dominates demand due to advanced semiconductor ecosystems and massive telecommunications rollouts. Southeast Asia, including Singapore, Malaysia, and Vietnam, is emerging as a manufacturing and design hub, contributing growing volumes of mid‑range secure FPGAs. South Asia, particularly India, is accelerating adoption in defense and automotive sectors. Oceania, with Australia and New Zealand, focuses on high‑end secure solutions for critical infrastructure and research. Each sub‑region’s growth aligns with the overall 9.28 percent CAGR trajectory.

Who are the leading companies in the Asia Pacific FPGA Security Market and what strategies do they employ?

Leading companies include Efinix, Inc., Flex Logix Technologies, Inc., Intel Corporation, Lattice Semiconductor Corporation, Microchip Technology Inc., QuickLogic Corporation, S2C, and Xilinx, Inc. These firms pursue strategies such as expanding secure IP portfolios, forming joint ventures with local system integrators, investing in regional R&D centers, and obtaining security certifications (e.g., Common Criteria, FIPS) to meet government procurement requirements. Product launches targeting low‑power edge security and high‑end data‑center acceleration further differentiate their offerings.

What does a Porter’s Five Forces analysis reveal about the Asia Pacific FPGA Security Market?

Porter’s Five Forces assessment indicates moderate threat of new entrants due to high capital and IP barriers, strong bargaining power of buyers like telecom operators and defense agencies who demand certified solutions, and moderate supplier power as foundry capacity remains concentrated. Competitive rivalry is intense among the eight key players, driving continuous innovation in secure architectures. The threat of substitutes is low, as alternative hardware security modules lack the reconfigurability and performance density of secure FPGAs.

What are the strengths, weaknesses, opportunities, and threats identified in a SWOT analysis of the Asia Pacific FPGA Security Market?

Strengths include a robust base of semiconductor talent, strong government support for secure technology, and established supply chains. Weaknesses involve high design complexity, limited standardization across countries, and talent shortages in advanced security verification. Opportunities stem from expanding 5G, AI, and autonomous vehicle markets, plus rising demand for hardware root‑of‑trust in cloud services. Threats encompass geopolitical trade tensions, evolving cyber‑attack techniques targeting programmable logic, and potential regulatory fragmentation that could increase compliance costs.

How does the value chain operate within the Asia Pacific FPGA Security Market?

The value chain begins with IP core developers and secure architecture designers, proceeds to FPGA manufacturers (e.g., Intel, Xilinx, Lattice) who integrate security features into silicon, then moves to assembly and test houses, followed by system integrators and OEMs embedding secure FPGAs into end products across telecommunications, data centers, defense, automotive, and industrial sectors. Distribution channels include direct sales, regional distributors, and cloud‑service providers offering FPGA‑as‑a‑service. Each stage adds security validation, certification, and lifecycle management to ensure trusted deployment.

What are the key investment insights for stakeholders in the Asia Pacific FPGA Security Market?

Investors should prioritize companies with proven secure IP portfolios, strong regional partnerships, and clear roadmaps for high‑end and mid‑range FPGA security enhancements. Funding R&D in side‑channel resistant designs, secure boot firmware, and automated certification tooling offers high return potential. Strategic acquisitions of niche security startups can accelerate time‑to‑market. Additionally, investing in regional fabrication capacity and talent development mitigates supply‑chain risk and aligns with government incentives for domestic semiconductor sovereignty.

What are the concluding takeaways for the Asia Pacific FPGA Security Market?

The market is on a clear growth trajectory, expanding from 1.27 billion in 2026 to 2.36 billion by 2033 at a 9.28 percent CAGR, driven by escalating security demands across diverse verticals. Segmentation by end user, technology, and configuration reveals multiple high‑growth niches. Competitive dynamics favor firms that combine deep security expertise with scalable manufacturing and strong regional alliances. Stakeholders who invest in certified secure IP, talent, and ecosystem partnerships will be best positioned to capture the expanding opportunity.

What research methodology underpins the analysis of the Asia Pacific FPGA Security Market?

The research methodology combines primary and secondary approaches. Primary research includes interviews with senior executives, product managers, and security architects from the eight key companies and major end‑user organizations across the region. Secondary research leverages industry reports, government publications, patent filings, financial statements, and trade association data. Quantitative modeling uses market sizing techniques, trend extrapolation, and CAGR calculation (9.28 percent) to derive the 2026 base of 1.27 billion and the 2033 forecast of 2.36 billion. Data triangulation ensures accuracy and consistency.

What is the scope and limitation of this Asia Pacific FPGA Security Market research?

The study covers the period 2025‑2032 with a focus on the Asia Pacific region, encompassing all major end‑user verticals, technology types (SRAM, flash, antifuse), and configuration tiers (low‑end, mid‑range, high‑end). It includes market sizing, segmentation, competitive profiling of the eight listed companies, and strategic analyses (Porter, SWOT, value chain). Limitations are confined to publicly available data and executive insights up to the research cut‑off; proprietary internal forecasts and unpublished contractual details are not disclosed.

Which key companies are active in the Asia Pacific FPGA Security Market and what recent developments have they announced?

Key companies include Efinix, Inc., Flex Logix Technologies, Inc., Intel Corporation, Lattice Semiconductor Corporation, Microchip Technology Inc., QuickLogic Corporation, S2C, and Xilinx, Inc. Recent developments feature Intel’s launch of a high‑end secure FPGA family with integrated tamper‑resistant key storage, Xilinx’s partnership with a leading Asian telecom operator to co‑develop 5G‑secure baseband solutions, Lattice’s introduction of a low‑power flash‑based secure FPGA for automotive gateways, and Microchip’s acquisition of a regional security IP startup to bolster its antifuse portfolio. These moves underscore the competitive pace and innovation focus within the market.